If you have a teenager in the house, you’re likely to hear the expression,”that’s the stupidest thing I’ve heard in my life.” A few things come to mind, “I guess you haven’t listened to some of the people I worked with,” is one, but I can’t keep from saying,”make a list and see if the next stupid thing you hear actually tops it, and so on.”

When it comes to the mistakes investors make, I’m sure the list is long. It probably starts with spending more than you make which results in simply not saving at all. Then comes not saving nearly enough because most people don’t actually go through the exercise of calculating their retirement needs. For those actually investing, a major error is the propensity to buy high and sell low. I wrote about this in Disappointing Returns sometime ago and described how for the 20 years ended Dec. 31, 2006, the average stock fund investor earned a paltry 4.3 average annual compounded return compared to 11.8 percent for the Standard & Poor’s 500 index.

More recently, we discussed Frontline’s The Retirement Gamble, a PBS broadcast that focused on cost, how a 2% fee in one’s 401(k) would wipe out nearly 2/3 of your returns over time. If you use an advisor and find that his (or her) personal advice is worth a fee, that’s a different story. I’m strictly talking about ETF or mutual fund expenses. That said, I present you with the stupidest thing I’ve heard a financial author say. Ever. This may change, of course, but it’s the benchmark against which I’ll hold other foolish quotes I find for the rest of my life.

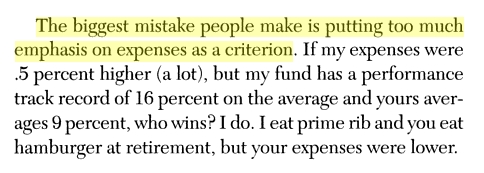

This is from David Ramsey’s Financial Peace Revisited. And I’m a bit taken aback. There are two implications here. First, that there’s a positive correlation between expenses and returns, as if to say “you get what you pay for.” This was disproved years if not decades ago. The second, and even more dangerous implication is that 16% is a number that one can ever see long term. The 80’s and 90’s (remember those years?) brought us a whopping true compound return of 17.99%/yr. But, of course the next decade’s fiasco brought the 3 decade average down to 11.29%. A look further back brings us closer to an even 10% CAGR. 10%. Not 12%. And certainly not 16%. Consider, at 16%, investments double in 4.5 years. 45 years would result in 10 doubles or your investment growing 1000 fold. Imagine putting $1000 away each year for your 10 year old knowing that starting at 55, she’d be able to withdraw $1,000,000 each year. Sorry, not going to happen. And when it comes to finance, hyperbole has no place in the discussion.

Sorry, Dave, expenses matter, .5% per year over one’s investing lifetime adds up to a sizable fraction of their account. Hopefully, you’ll have the patience to understand this and withdraw these remarks that can damage your followers’ hard earned savings.