Last February, I asked the question – Are you 401(k)o’ed? I was concerned that my readers might not have been aware of the fees they were paying inside their 401(k) retirement accounts. It seems that this topic has hit the mainstream media, and recently, PBS’ Frontline ran their story The Retirement Gamble which you can see on line if you missed it.

The message is simple, over time, fees will destroy your returns. Over a lifetime of investing the difference between a .1% cost and a 2% cost is insane.

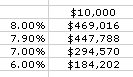

Jack Bogle, the father of index investing, is interviewed and discussed these numbers, how the market might grow your $10,000 to over $45,000 over 50 years at 8%, but a 2% per year cost will confiscate nearly 2/3 of your returns. Unfortunately, Jack misspoke when he said, “Get Wall Street out of the equation. Get trading out of the equation. Get management fees out of the equation. You own American business and you hold it forever. That’s what indexing is. Own a fund that owns the entire U.S. stock market, does no trading, and has a cost of 1 percent a year to own. And that is the only way to do it. Then you’re with a creature of the market and not of the casino.” Even 1% isn’t great, you’d still lose 1/3 of your money over the five decades in his example. A tenth of a percent is more like it. Over the years, there’s still a $20,000 loss to fees, but we’re talking 50 years in the example. The quote got it right, but I think Jack meant to say a tenth percent.

It was decades ago that Jack Bogle promoted the concept of indexing and founded Vanguard’s Indexed Mutual Funds long before ETFs were invented. Anyone who has any background in finance and investing would be aware of Bogle, Vanguard, and Bogle’s thesis that managed funds can’t add enough value to exceed their high costs.

Everyone except for Christine Marcks, President, Prudential Retirement who responded with, “Yeah, I haven’t seen any research that substantiates that. I mean, it— I don’t know whether it’s true or not. I honestly have not seen any research that substantiates that.” The interviewer asked if she’d seen the research Vanguard had done on the topic and she replied, “No, I haven’t. I haven’t— I haven’t read everything. But so much of it depends on, you know, what I need is different than what you need and there’s not an asset allocation or a fund strategy that’s right for everybody.”

One last quote from Jason Zweig of the Wall Street Journal, “And one of the ultimate dirty secrets of the fund industry is that a lot of people who run other fund companies own index funds in their— in their own accounts and don’t talk about it, I mean, unless you put a couple beers in them.” I suspected that, myself.

To be fair, not all 401(k) funds have such high expenses, the S&P fund in my own 401(k) is .06%, less than a 3% hit over 50 years. Frontline also missed, or ignored, any discussion of matched funds. My own advice is when your company offers a dollar for dollar match, you should grab it. The decades pass quickly and you’ll look back at a high six figure account and see how nearly half the money came from your employer instead of from your wallet.

Check out the show and let me know, did you feel it was balanced? Was I too tough on Christine Marcks? Have you check the fees inside your own 401(k)?

I just watched that documentary the other night. I completely agree that indexed mutual funds are the way to go. When I hear that people trade single stocks and still have debt, I try to point out that it is such a gamble to do this especially if this is money that is put aside for retirement.

My work 401(k) plan has really high fees (1% for some funds, well over 2% for others). It drives me crazy, but I gotta take advantage of that 3% match.

It’s for this reason that most of my investing is done in Vanguard and with index funds (with some play money in stocks I choose).

That’s it! If there’s any chance you’d be at that company over 7 years or so, the 1% is a killer.

Depositing just the 3% to the match makes sense. Then those index funds can grow and only have a cap gain rate when you sell. Thanks for writing in.

Joe as someone who advises a number of plans and serves as advisor to a number of individual clients as well, much of what I saw wasn’t new to me. That said, the show clearly had an agenda which hindered the effectiveness of the message. Yes fees are an issue, but they failed to highlight individuals who have used their 401(k) to amass a sizable nest egg or any plans with a mix of active and passive choices that offer excellent fund choices and keep costs low. Not to toot my own horn but I could connect them with clients in both camps.

I am a huge fan of indexing and use index products in my practice extensively, but not exclusively. I’ve found that saying it is always one way in the field of investing and personal finance is rarely a good idea. Solid actively managed funds are harder to find and take more work, but that is what clients pay competent advisors to do.

Ms. Marcks was at best poorly prepared for her interview and at worst a complete moron.

Roger, I appreciate the visit and comment.

You got me thinking now – with [Frontline having] nothing positive to say, I wonder how many viewers will simply be scared away from an otherwise good 401(k) account. Or miss the match that would negate the otherwise bad fees.

I worked with a guy that would check his account every day and buy whatever was hot. He lost money as he was day trading with his 401K, WRONG!!!

Indeed, wrong. What a shame, thanks for the comment!