The book “Last Chance Millionaire” by Douglas R. Andrew was interesting to me, if only for the lack of depth. It reminded me of the original “Twilight Zone” TV series in this regard – every episode could be summarized in about three sentences or one minute of action, and the remaining 24 minutes was filler.

Mr. Andrew spends the first 200 or so pages making the case that one should always have a mortgage, and it should be as large as possible. Now there’s a premise I’d not want to spend too much time debating, but I’d agree that there are better times to borrow and other times to pay down one’s debt. I am old enough to remember a 30 year fixed rate of 13.5% which, in the 25% bracket is still 10-1/8% after tax. At that rate, I prefer to pay down the mortgage and advise other to follow. With rates below 6%, someone in the 28% bracket has an after tax interest cost of 4.32%. There, I just saved you 200 pages.

He goes on to suggest investing in Indexed Universal Life Insurance. I am on record as being anti-variable annuities, but this product offers a few different twists. The withdrawals are first made against the principal within the account, so no taxes are due. Then with a bit of smoke and maybe a mirror or two, further withdrawals are taken as ‘loans’ against the account, which are then paid back on death.

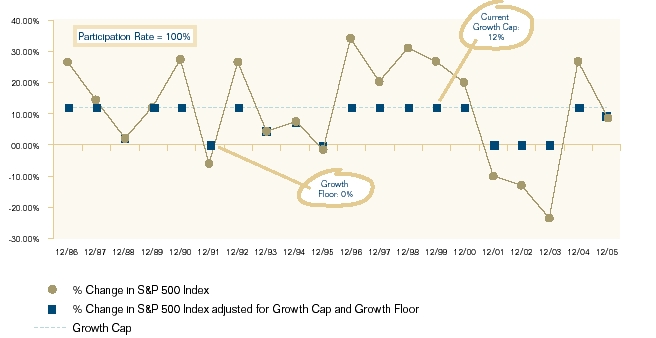

I wanted to find out how the account grows in value and discovered a policy by Pacific Life called “Pacific indexed Accumulator II” which describes the annual crediting. One receives the return of the S&P index (no dividends) with a maximum of 12%, and minimum 0%. So the trade-off appears to be that you give up the dividend (The S&P currently yields about 2.1%) as well as accept a cap of 12% per year, in exchange for a guarantee of no annual losses. I’m still on the fence about borrowing to fund this, but the concept itself has a certain appeal. This chart from the prospectus does a good job illustrating the return you would have gotten over the past 20 years. I thank one of my regular readers for bringing this book and investment approach to my attention.

Joe

Based on the crediting method of the PacificLife Index Accumulator you can get 114% participation rate.

Not seen this product. Do you have access to the full prospectus?