A few weeks ago, I talked about the end of estate planning. It might have been a bit of an over-reaction to the news that the estate exemption was made a permanent, inflation-adjusted figure of $5.25M for 2013. Perhaps I was jumping to conclusions as there are a number of reasons one may want a trust. More important, you may have done some advanced planning years ago when the $1M exemption wasn’t enough to keep your estate (death) tax free.

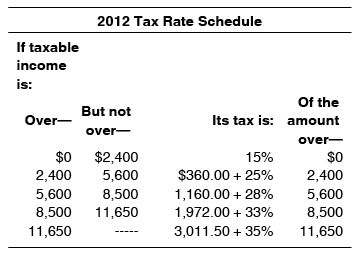

You may have discovered, however, that income retained within that trust is taxed at some pretty crazy rates;

This, as compared to a single filer that would not hit 28% until a taxable $85,650 or married couple filing jointly at $142,700. Fortunately, in 2013, there is still a long term capital gain rate, albeit a higher one, 20%, plus 3.8% if the trust is in the top bracket. Nearly 24% when the trust beneficiary may very well be in the 15% bracket.

How to navigate this? First, you need to consider whether the trust should retain all of its earnings or if the beneficiary is responsible enough to get this small distribution. In 2013, a child subject to the ‘kiddie tax’ can receive up to $1000 in unearned income and pay no tax. Additionally, the next $1000 is taxed at the child’s rate, likely 10%. If the trust assets are loaded with CDs earning interest, this may be tough, as interest is all taxed at the ordinary rate. Invested in the right mix of low dividend stocks would keep the need to distribute any income to a minimum.

Even with the generous estate tax rules currently in place, a trust can help your heirs avoid probate, and in case you have a child whom you fear would blow his inheritance on a weekend in Vegas, the trust can be used to provide an annual stream of income instead of a lump sum windfall.

1. Yes, I still have a Trust.

2. Yes, the Trust tax rates are obnoxious.

3. But mine is strictly an Avoid Probate Hassles strategy. And as a revocable inter-vivos trust, its income is included in our normally taxed joint tax return. So until we both die, the Trust tax rates are a non-consideration.

thanks.