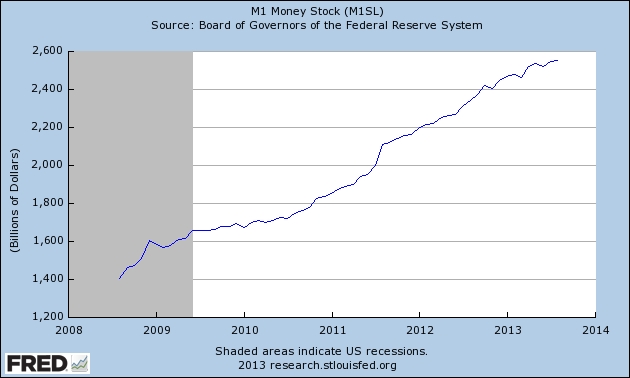

We talked about the Taper, today, I’ll share my bigger concern, the potential wave of inflation. We first need to understand a couple things. First, a look at M1 –

From the end of the recession, M1 (Defined as “M1 includes funds that are readily accessible for spending. M1 consists of: (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) traveler’s checks of nonbank issuers; (3) demand deposits; and (4) other checkable deposits (OCDs), which consist primarily of negotiable order of withdrawal (NOW) accounts at depository institutions and credit union share draft accounts.”) has gone up by a Trillion Dollars, or over 60% in just about 4 years. This doesn’t tell the whole story. We need to look at Velocity –

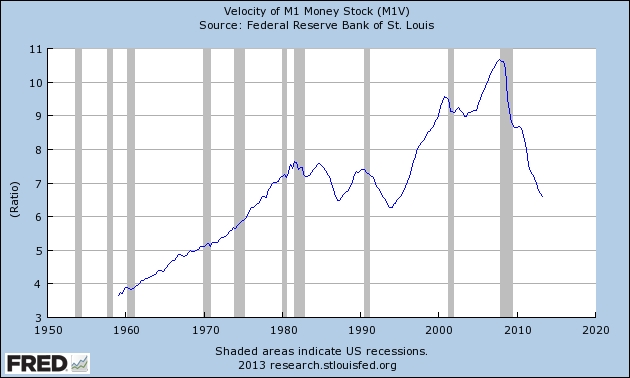

Velocity is the reason why the required money supply doesn’t need to equal an entire year’s GNP. It’s defined as the average frequency with which a unit of money is spent on new goods and services produced domestically in a specific period of time. The time unit is nearly always defined as one year. So, we stare at the growth of M1, but see that velocity has tanked. We exited the recession with about $1.6T in ‘cash’ times about 9 giving us a result of $14,4T. Now, M1 is nearly $2.6T, but velocity has dropped to 6.5 resulting in $16.9T. Barely a 17% increase over 4 years time. (Note, GNP is running at just over $16T for the year, so my eyeballing the numbers here is resulting in a bit of rounding error.)

I don’t know when the economy will gain some steam, but it will happen eventually. When that happens, velocity will go back to more normal levels, and that will potentially create a wave of inflation that will catch many by surprise. But just as the banking crisis was predictable, so is this. The only way to avoid a highly damaging level of inflation is for the Fed to quickly drain excess liquidity. So as we move forward, the money supply is an important part of the equation, but don’t take your eye off velocity. It’s the indicator that will tell you whether the Fed has to act, and act fast.