A fellow blogger wrote about the debt snowball. For those of you who do not know what the debt snowball is, it’s a method of paying one’s debt off (a good thing) ordered from lowest balance to highest. I wrote about this over 7 years ago when I was Thinking about Dave Ramsey. In that article, I was trying to keep an open mind. I’ll even suggest that for the lost few hundred dollars, if the good feelings you get from knocking off the first card help keep you going, a few hundred, or even a thousand dollars might be a small price to pay for long term success. In my opinion, the fastest way to eliminate all one’s debt is simple – make all minimum payment due, and send any extra money to the highest interest debt. Others insist on the snowball good feelings.

But. As a numbers guy, I ask, “Where do you draw the line?” And toward that end I wrote to Derek, the blogger I mentioned –

“I don’t dispute that killing off a card completely can provide an emotional reward, a boost to one’s feeling of accomplishment, etc. But, I often say “knowledge is power” and one should know the cost of that decision. A few hundred dollars over 4 years? No big deal. Thousands of dollars? Look carefully at the numbers before choosing the method.

Consider “snowballers” suggest you pay your 8 student loans, all zero interest, $10,000 each, before paying that $20,000 18% card. Of course, that’s an exaggeration, but one that easily illustrates why it’s important to look at the numbers.”

What I expected was an acknowledgement that there are some extreme, contrived, cases when you just pay off that 18% debt first. Nope. His response?

“I used to be like you “a hard-nosed financial professional that only believed in the numbers and percentages. Today, I understand much more about the emotional side of money. If you make no progress over the course of a year, there’s about a 100% chance of giving up. If, however, you pay off a $2,000 loan and get rid of that payment completely, you’ll be charged up and ready to tackle another!

I’d still suggest that people pay off their $10,000 zero interest loan before their $20,000 18% interest loan because there’s a greater percent chance of them getting rid of the smaller debt and continuing their debt payoff journey! Pay a couple thousand extra dollars in interest but paying off the debt is better than trying to save the interest and failing at the debt payoff entirely, don’t you think??”

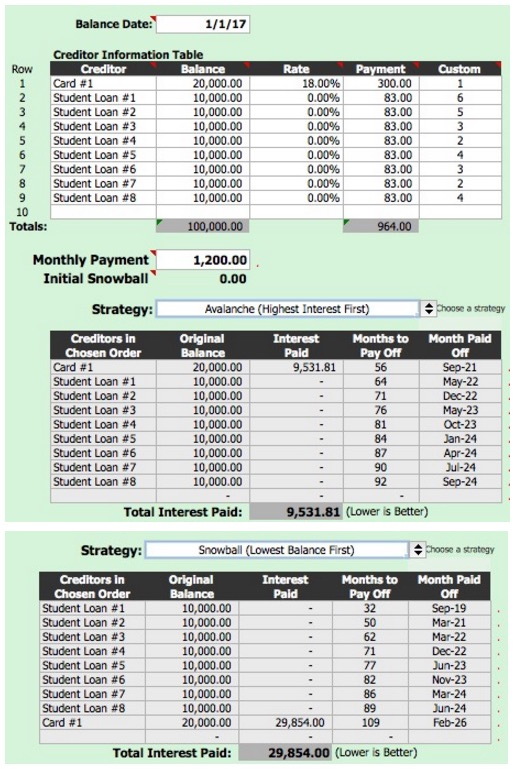

What? I aimed to find the most ridiculous spread from high rate to low, trying to show how there’s some point where it’s silly to pay off your low-to-no interest debt first. And, with a daughter about to enter college, I figured that an example of 8 low rate separate loans was actually possible. Here’s what this would look like. Do you see what makes this so ridiculous? You graduated college, and the loans happen to be individual loans. The lender could just as easily have made this into one loan with a monthly $664 due. In which case, the snowballers would have no issue paying the “low balance” $20,000 card first. But because these loans are each $10,000, they rise to be the priority, pay them off, get rid of 1, 2, 3, etc as fast as you can, before sending an extra dime to the $20,000 high rate loan.

Let’s look at what happens when we prioritize that awful 18% debt. I happen to choose a total $1,200 available to pay debt, just $236 more than the minimums required. If we pay the low balances first, the interest jumps by over $20,000. A $10K loan is too small to kill in less than a year with only the $236 extra, so the snowball takes 32 months to eliminate one debt, while my plan gets rid of the credit card 18% debt in 56 months. Would you really be happier paying interest-only for 89 months on that 18% debt but feeling great that you have fewer loans, fewer checks to write?

The truth is that most people are not in such an extreme situation. And the real cost may be far less that this contrived example. As I offered on Derek’s site, knowledge is power. Why would you not wish to know the cost of one method vs another? And if you knew the cost, how high (or low) would it need to be to sway your approach to paying off your debt? What could you do with the $20,000 you’d have saved over these 10 years? How much snowball Kool-Aid does one have to drink to state they will stick to a method no matter the cost?

By the way, I do believe in more than numbers and percentages. I also believe one shouldn’t fall for bad advice offered by a celebrity, Dave Ramsey, who takes a “my way or the highway” approach to his advice. Know your options, and decide for yourself.

On a final note, as I was writing this, John, another blogger who writes at Military Fire, also visited Derek’s article, and agreed with me, stating,

“If the snowball method costs you a couple thousand annually, and you make less than $50K a year, you would have to work 13 months a year to recoup that unnecessary interest. The snowball requires nuance. Lets help people work smarter, not harder.”

Derek, on the other hand, wasn’t budging,

“I’m a nerd just like you and understand the percentages perfectly. After helping hundreds of people though, there’s no denying that those who pay off a debt early are far more likely to stick with their debt snowball. To help the most people possible, I’m sticking with this method for life.”

Check out John’s excellent article Debt Snowball: Not a Chance in Hell, because John doesn’t like throwing away money on interest any more than I do. If you comment at either site, let them know that Joe sent you.

You’re right.

Usually, the snowballer’s are right too, though – smaller debts tend to have bigger interest rates.

If you’d roll all those student loans into a single line-item, snowballers would have the right advice again.

Nice site!

Hi Aaron! thanks for the visit and comment. We all have different experiences. When I was younger (35 years ago), it was common for the best cards with low rates to also give a low credit line. My original comment to Derek was just poking the bear, trying to see if a hardcore snow-man would change his tune given a worst case example. I got my answer. You are right, if the 8 zero interest loans were consolidated, the snow-men would then pay high interest first. This make sense to you?

I’m not a fan of the snowball route either. Attacking the debt with the largest interest always provides the best rewards. It’s common sense.

Ken, I appreciate the support. It’s remarkable to me that when you compare the two ways to pay this off, one has about $10K in interest, the other, $30K. I’m the first to say, “If the difference is minimal, and you’ll sleep better knocking off a few cards with low balance, I won’t argue.” I find it amazing how Derek and others won’t give an inch, even when $20K is at stake.

Yea I agree 100% folks have to consider the reality of the situation. There are other ways to motivate yourself. I have a problem with the dave Ramsey style… also the credit card issue. …. The fact is if you don’t have a cash back credit card that you take advantage of then you are losing plain and simple. CC companies drive up the cost of goods and services. If you aren’t getting checks every year from the rewards then you are the one funding those reward programs. That is how I see it.

Agreed. The merchant pays the card fees regardless of whether I get my rewards. And those fees add up so fast that the card issuers are in competition with each other to gain us, the card user, as customers. I often wonder, if we all just said we don’t need the rewards, could we drive down the merchants costs? And if so, would we see lower prices at the stores?

The only way to drive down prices is not by saying no to rewards…. its done by saying no to cards. The other way would be for merchants to charge a fee for the privilege. Until then you are either winning by taking advantage of the rewards or losing by financing those that do.

Nerds work on repeatable fact-based logic and reason, not subjective anecdotes. Therefore Derek is not really a nerd. He’s essentially suggesting you take it on his authority that the snowball method works. And to quote Albert Einstein: Unthinking respect for authority is the greatest enemy of truth.

Hi Joe,

I have a different reason for advocating paying smaller loans off first, even 0% interest and eating the interest cost. This one isn’t quite an emotional reason, but one that I think is critical for a lot of people with multiple debts looking for advice. Cash flow. No matter how low your interest rate, your loan still has a minimum monthly payment that you must satisfy. Paying off the smaller loans first increases your monthly cash flow by that minimum rate. That gives you a greater financial cushion to deal with emergencies or put towards other loans. If someone is at a point where after paying all their bills and monthly minimums, they have very little left to put into savings or use for luxuries, I feel that prioritizing smaller debts is the smarter strategy. It costs them more, but gets them to the point where they can weather financial emergencies faster.

Saving $10k in interest does you little good if causes you to incur debt that will end up costing you the same or more in the process. A lot of debt advice seems to assume or require perfect financial behavior and adequate emergency savings. That’s simply not a good assumption for many people. Your model in this blog doesn’t seem to account for this.

Keep one thing in mind. I do not consider myself an anti-snowballer. I am, however a math guy. This post came from a discussion at another blog, where the author made the point that, just like Dave Ramsey, there’s no choice, no discussion. I tell my readers to be aware of the numbers and decide. In my contrived example, the cost is huge, and I remain incredulous that anyone would advocate paying off a series of 0% loans while they still have 18% debt.

The issue you raise is different. Freeing up one credit card may very well set the stage for some responsible usage, and recapture the grace period. In the real world, the difference from high rate to low will not be so wide, and your strategy will likely have minimal cost. You see? I’m fine with whatever you choose, so long as you consider all options, and made your own decision.